The idea that there is, or could ever be, one set royalty for all formats is a fantasy perpetuated by industry outsiders who have little idea how the business of publishing operates. Author and publisher compensation varies according to platform, audience reach, production costs, which country the sale is in, and a host of other factors.

In the world of unlimited digital book subscription there’s much speculation about how much a publisher will earn from a read or listen, and a general consensus is that said read or listen will generate less revenue than an à la carte sale.

For some this is enough to decry subscription as a negative force in publishing, but all too often the negativism is either ill-thought-out or simply self-serving, coming from parties with vested interests in models created and sustained in an era before digital subscription was viable.

The classic anti-subscription argument conjures up microscopic payouts such as we see from music subscription services like Spotify, always conveniently overlooking the fact that a typical music download may be just a few minutes long, while a book may run to hundreds of pages or many hours of listening, making meaningful comparisons all but impossible (not that the anti-subscription brigade ever let rational argument get in the way of a faux narrative!).

Earlier this month Sweden’s trade journal Boktugg revealed the Q4 payout numbers for Sweden-based Storytel, the world’s leading unlimited audiobooks subscription operator, and with that we have fresh insights into how much publishers (and by extension authors) might be getting, at least in Sweden.

That matters because Sweden is, by far, the largest unlimited subscription market for books on a per capita basis, and Storytel is not just the largest operator in that market, by far, but also the mostly globally engaged, actively operating in 26 markets as this post goes live.

Obviously we cannot make direct comparisons with publisher payouts in Sweden compared with say, the USA, but the broad narrative is instructive.

A look at those Storytel numbers shortly. First a more general discussion on the nature of author compensation, where again I can draw on Boktugg’s Sölve Dahlgren, who kindly ran a summary of an article published by Sweden’s Dagens Nyheter (DN) which carried dissenting voices from the Swedish author community. The Boktugg post offered insights that helped clarify my understanding of the DN post, which Dahlgren summed up as trying to,

Shed light on different aspects of the audiobook discussion (but that) felt a lot like a tired repetition and that we did not really get that much wiser.

That’s a feeling anyone who reads the UK’s The Guardian’s coverage of the publishing industry will share, but let’s stick here with the DN article.

The DN post interviewed 22 authors, quoting 14, so two-thirds, and from that we might reasonable expect some valuable insights into the state of author-subscription relations in Sweden. The conclusions therefore surprised me when I first read the DN post, because there was a negativity about subscription that generally does not come across in the debate about subscription in the Nordics.

Dahlgren’s local knowledge was able to pinpoint why:

Most surprising, however, was the selection of authors. None of the interviewees are (what I could find) among the most listened to at Storytel, Bookbeat and Nextory last year. In other words, DN has not interviewed any of the authors who belong to the winners. (Although, for example, Mats Strandberg and Malin Persson Giolito have books that have definitely been listened to diligently). One of the interviewees does not have any audiobook at all at Storytel.

(Bold text reflects correction after advice on translation from Mr. Dahlgren.)

But DN’s post was not just about royalties but had a wider agenda.

Staying with Dahlgren’s summary:

The authors had a mixed view of audio books. Some expressed that they are not interested in changing the way they write to make their books fit as audiobooks, while others said that a good text does not require adaptation to become a good audiobook.

Both perspectives are valid, depending on how we define audiobooks.

If we are looking for a book read out loud by a competent voice artist then the latter perspective holds true, and this is very much the audiobook standard right now. Books are, with very few exceptions, written to be read. Whether internally in silence or out loud to an audience is really neither here nor there. A well-written book should and does work both ways, so long as the out-loud narrator does his or her job well.

On the other had we have books written for audio, which we see exemplified in the “Originals” (the upper case ‘O’ is de rigueur) produced by audiobook companies where authors are commissioned to write books to be heard. Some may not even be available as a text alternative.

These are two separate sets of writing skills and not all authors will be comfortable with both, and that’s fine, of course. The beauty of the newly refreshed audio market is that it opens up new possibilities for audio-first authors that for practical reasons (production and audience reach) were not meaningful ten years ago. One more example of the Global New Renaissance unfolding.

Okay, so let’s return to what this post is really about: money. Because at the end of the day this is what drives the platform, the publisher and the author.

First we need to consider author compensation in general terms, and distinguish between author royalties and payouts to publishers, which are not the same thing, although the distinctions are blurred on platforms like Kindle Unlimited, the unlimited ebook subscription service offered by Amazon.

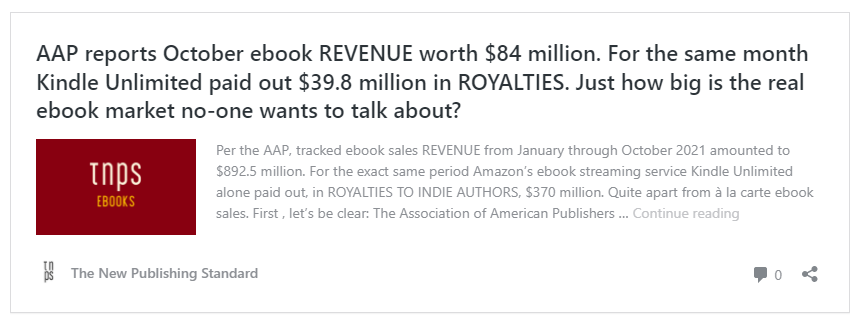

In the latter case it should be noted that Kindle Unlimited pays outs serious money every month (monthly, not quarterly!) to “indie authors”.

Serious money? Try just shy of $40 million, paid out to self-publishing authors for ebooks downloaded through Kindle Unlimited, in just one month, October 2021. (Watch out for a near-future TNPS update with the full 2021 payout.)

UPDATE: In 2021 Amazon’s Kinde Unlimited paid out $450.1 million to its self-publishing authors for downloads through the service.

Of course these are not really “royalties”. By definition self-publishers are not being published by Amazon or any other third party, so the Kindle Unlimited pot payout is actually the indie author equivalent of the payout to publishers on Storytel. With the Storytel payouts, of course, the payment goes to the publisher and from that payout the publisher hands over the contracted royalty to the author.

Both Kindle Unlimited and Storytel operate a similar model whereby the collected revenues from subscribers are shared out between platform and publisher/self-publisher. Per Boktugg the Storytel-publisher split is routinely 50-50 (bigger publisher contracts may strike better deals). That is, 50% to Storytel, 50% to the publisher (not author). For Kindle Unlimited the share ratio is known only to Amazon, and Amazon announces its total pot payout each month after the fact.

What vexes authors (and publishers who claim to have the author’s interests at heart), is that the payout from the platform determines the actual royalty the author finally receives. And both authors and publishers struggle sometimes with how much that royalty ought to be.

Should the royalty for an audiobook be the same as for a paper book? I would argue no, because the production costs of the audiobook are substantially above that of an ebook, which often may just be a digitised version of a printed book.

Which begs the question should an ebook royalty be the same as for a paper book? Should different paper formats carry the same royalty?

The reality of course is that authors have long since been paid varying royalty rates according to format and indeed according to audience reach, so when authors are asked to accept a different, and usually lower, royalty rate for subscription, there’s nothing new here in principle.

Yet as we know, the world’s biggest trade publisher, Penguin Random House, famously (and without consultation with its authors, although it did attempt to dress up the move as being in its authors’ best interests) pulled all its titles from all unlimited subscription platforms citing low royalties. Let me return to that shortly.

Sölve Dahlgren took up this topic of variable royalties too, in his insightful post on Boktugg, so let me bring in the Swede’s perspective here:

It is true that the compensation for an audiobook (or ebook) that is consumed via a streaming service is lower than for a paper book. But at the same time it has a longer lifespan. And just like with bookshops and book clubs, lower prices lead to higher consumption.

One might of course add there libraries and digital libraries, etc. So to be clear, the idea that there is, or could ever be, one set royalty for all formats is a fantasy perpetuated by industry outsiders who have little idea how the business of publishing operates. Author and publisher compensation varies according to platform, audience reach, production costs, which country the sale is in, and a host of other factors beyond the scope of this essay.

Widening this debate, then, an author can, by choosing to self-publish on platforms such as Amazon’s KDP or Kobo’s KWL or a host of other options (direct to Apple or Google Play, or by using an aggregator to reach myriad others), collect an ebook royalty as high as 60%-70%. They can also see that 70% payout drop to a relatively measly 35% if they choose to price their books outside the price schedules the platforms set.

Curiously when Penguin Random House pulled its titles from the unlimited platforms citing its authors best interests it did not at the same time pull its titles from à la carte ebook platforms because the authors were getting paid far, far, far less than the possible 70% they could be getting.

And as noted here in previous TNPS discussion about subscription, by removing titles from these platforms PRH determined that its authors, instead of receiving a small percentage of something from being available on these platforms, instead received a whopping 100% of nothing from these platforms.

The double standards are evident too in the indie publishing world where some indie authors rant at traditional publishing royalty rates, citing the 70% they can get from KDP, while quietly using the KDP’s paperback production option where they accept, again very quietly, a far lower royalty rate, or running low-price sales that mean they only get a 35% royalty. Repeat for audio where Amazon-owned Audible’s self-publishing arm ACX is notorious for its low royalties to indie authors, both for à la carte and for Audible’s own unlimited subscription service.

The moral of this little digression being to reinforce the point made by Sölve Dahlgren, that royalties have, do, and will vary enormously and this is a normal part of the publishing landscape.

With subscription we add yet another variable – royalties can vary month by month (Kindle Unlimited, for example) or more usually quarter by quarter, at the whim of the platform as determined by data and insights only the platform knows.

At which point let’s bring in Mr. Dahlgren yet again, for his insights into Storytel’s royalties schedule for Q4 2021.

To be clear: the Storytel payout varies each quarter, being based on how much revenue comes in from subscribers shared against how many pages are read or hours listened to. We need too to bear in mind these numbers are for Storytel Sweden, and the rates will be different in other markets (and from other platforms). And we need to allow that some publishers may get preferential or less preferential rates depending on their negotiating power. Some bigger publishers may even get paid a fixed rate per download, but the usual MO is a share of the pot, and that’s the focus here.

This is what we know:

Storytel Sweden’s Q4 2021 per hour rate, divided usually equally 50-50 between Storytel and the publisher, with caveats as above, was SEK 4.32 ($0.47), meaning a typical publisher collected per hour the princely sum of $0.23, or $2.30 for a ten-hour audiobook.

How much the author then gets, if not themselves the publisher, will depend on the author’s contract with the publisher, and so a separate consideration.

As mentioned above, the rate varies per quarter dependent on external factors, but Boktugg tells us the Q4 2021 payout was more than for Q3 2021 – $0.22 – but less than for Q4 2020, when publishers typically received $0.25.

So far so bad, one might argue, comparing rates with the US average audiobook retail price and percentage royalty, but that of course is a tenuous argument assuming all other actors and factors are equal.

What really matters here, rather, is not the hourly rate per se but how many eyes or ears are on those books each month.

And that of course reflects the reality of publishing in any format. Put simply, it is nonsensical to argue, as I see some authors do, that their book is worth (example only) $5 and that they will not sell for $1 because that demeans their work and they cannot afford to live, let alone write, at the lower price.

It is meaningless because no author lives on a payout of $1, $5, $10 or even $1,000 dollars. The unit price is not the issue. JK Rowling is not rich beyond imagination because her books sell at crazy high prices. She is rich beyond imagination because so many of her books were sold at typical industry prices.

The same argument applies when authors and publishers eschew foreign markets because retail prices are low. China and India being classic examples. No, the unit return per sale is nowhere near the US level, but many western authors and publishers are comfortably well off from sales in these countries.

Expand that argument further to online reading, where again traditionalist western authors look on horrified at the payouts per unit, while enviously seeing top-selling authors on these online reading platforms raking in crazy sums.

Volume is what this publishing game is all about – at least, if you want to make a living from it.

And volume of course is where unlimited subscription, by removing price friction for consumers, comes into its own.

Sticking with Sweden, and in the US we love to talk about soaring audiobook growth, always conveniently overlooking the ebook growth of the early 2010s which was higher still. But the US is a big market, serving a population of 320 million people. Compare the ten million in Sweden.

What we are clearly seeing in Sweden, in the wider Nordics, and increasingly elsewhere, is publishers fighting to get their titles onto these unlimited subscription platforms – and by understanding at least some of the reasons why that is so we can make better-informed decisions about the unlimited subscription debate within the publishing industry.

First and foremost, subscription is the preferred consumer mode, as is self-evident everywhere where unlimited subscription is meaningfully available – just look at music and film/TV streaming.

The key here being “meaningfully available”. Many publishers in the key English-language markets are too busy defending the status quo of print dominance and bricks and mortar stores as (an understandable and justifiable) bulwark against Amazon to be able to step back and see, let alone embrace, the bigger picture.

The bigger picture being that when a meaningful choice of content is offered on an unlimited platform the consumers only concern is how many platforms they can afford to sign up to. Again, just look at film/TV streaming or music streaming. (And if you are in the anti-subscription camp for books, ask yourself how many music and video subscription services you are signed up to.)

But by deliberately keeping top-selling content off unlimited subscription books platforms publishers create a self-fulfilling prophecy, that so few consumers sign up to these unlimited ebook and audiobook subscription platforms that it isn’t worth the publishers while.

Yet it’s not rocket science to understand that the more quality content you make available the more consumers you will attract. In fact it’s so blindingly obvious as to almost make one think some publishing CEOs are being disingenuous when they assert these platforms are bad for authors.

I look forward to hearing Markus Dohle explain how 100% of nothing is better than x percent of the something that PRH authors were previously getting from platforms like Storytel. And let’s keep in mind that most Storytel markets could hardly be said to be cannibalising PRH print sales (Storytel did not at that time have a presence in any English-language markets except India and Singapore).

And that of course is yet another argument that wilts under scrutiny, because pretty much every report that rolls out shows unlimited digital subscription does not cannibalise print sales, and counter-intuitively may actually boost them.

One need only look at the results of the Pandemic years to see how print, audio and ebooks all rose together.

And that Pandemic-induced boom was not least because of backlist sales and downloads, derived from increased discovery, which just happens to be where unlimited subscription really comes into its own.

Let me pause here to bring in the UK’s The Bookseller, again from earlier this month, which reported on how backlist titles accounted for 58% of revenue from the top 50 earners in 2021.

With unlimited subscription, of course, backlist titles (assuming the publishers have bothered) are available 24/7 at no extra cost to the consumer, and without that price friction more books are read or listened to, and more consumers are subscribing, and for each read or listened to title that’s more revenue being lined up for pay day.

And staying with the thorny topic of price friction, the lack of same that comes as part of the unlimited subscription deal means consumers are much more willing to experiment with unknown author names and brands or even explore different genres they would never risk if paying a full and non-refundable retail rate.

It’s no wonder that in some countries authors and publishers are fighting to get their titles into unlimited subscription platforms and publishers even join forces to launch their own unlimited subscription platforms (as examples Chapter in Denmark and Fabel in Norway).

{kind=link}